Introducing Zeller for Startups.

Don’t waste time assembling disparate tools or waiting in line at a bank. Zeller for Startups is an all-in-one financial solution for founders, by founders.

Don’t waste time assembling disparate tools or waiting in line at a bank. Zeller for Startups is an all-in-one financial solution for founders, by founders.

Speak to our expert team about your in-store payments, and we’ll personalise a solution to your business and budget.

Enjoy a free, built-in POS system with the new Zeller Terminal 2. Order today with free express shipping nationally.

Starting a new business? Enjoy a free, built-in POS system with the new Zeller Terminal 2.

12.10.2023

The idea of asking customers to cover the transaction fee when they choose to pay via card is not new. We’ve all been in the situation where we’ve ended up buying something we didn’t need, purely to reach a business’s minimum EFTPOS requirement. The minimum card spend was introduced as a way for businesses to discourage customers from paying on card, so that they could avoid paying the transaction fee. At a time when people also held cash in their wallets, this practice made sense, but it’s fast becoming outdated, and frankly very frustrating. According to a 2023 report by the Reserve Bank of Australia, 76% of all payments in 2022 were made on card. It’s becoming increasingly counterproductive and costly for businesses to ask customers to pay with cash, and yet, someone still has to foot the bill for EFTPOS payments. This is where surcharging comes in.

Surcharging is more prevalent in service industries. In the food and drink industry our data indicates that nearly 60% of hospitality businesses have chosen to enable surcharging on electronic payments. This is followed by the transportation and beauty sectors where approximately 40% of businesses are choosing to pass on their transaction costs to the customer.

Before we get into the regulations surrounding surcharging, it’s important to understand how EFTPOS transactions work. When a customer uses a card or mobile wallet to make a purchase, a number of fees are charged between your bank (or payment provider), your customer's bank and the payment card network (eg. Visa, Mastercard, or American Express).

The fee that you are charged to process the payment is entirely dependent on the type of card your customer uses, and may range between 0.2% and 3.5% dependent upon which payment services provider you've selected. Additionally, your bank may charge you monthly EFTPOS terminal rental fees, account-keeping fees, or monthly service fees (learn more about The True Cost of EFTPOS Transaction Fees here). Together, these fees make up what is known as the ‘total cost of acceptance’, that is, the expense incurred to accept a card payment.

Unless you are using a service such as Zeller, which keeps things simple with one low, flat fee of 1.4% per card-present payment, it can be extremely difficult to calculate your cost of acceptance. Why this is important, is because, should you choose to pass on the cost to your customer, you legally cannot pass on a charge greater than the one you incur. In order to curb excessive surcharging, the Reserve Bank of Australia introduced the following legal obligations:

As a merchant, you have a responsibility to check your annual statement, to ensure your surcharge remains less than — or equal to — your cost of acceptance, and set your surcharge for the following year based on what you discover.

For Matt Bisaro, who runs Floral Craftsman in Sydney’s affluent suburb of Mosman, having one low, flat rate meant that he didn’t have to turn away customers wanting to use American Express, which traditionally incurs a much higher transaction fee.

“My favourite thing with Zeller was that I got the same [fee] for AMEX. I used to have to refuse AMEX payments, and I lost people over it… Now you can add on that surcharge and no one thinks about it.”

Matt Bisaro, owner of Floral Craftsman, Mosman, Sydney

As public perception around surcharging is not typically positive, it’s always important to tread with caution so as not to get customers offside. When weighing up whether surcharging is right for your business, consider the following:

After taking into consideration your industry, your location, and your customers, you might decide that surcharging is not for you, which is completely reasonable. However, avoiding EFTPOS transaction fees altogether is becoming increasingly difficult as customers move away from cash. It’s therefore more important than ever to reassess your EFTPOS solution to ensure you are getting the best deal. With Zeller Terminal, you can own your EFTPOS machine outright, and will only be charged one low flat fee of 1.4% per in-person card payment. No hidden costs, no lock-in contracts. You can also speak to the Zeller Sales team about an even lower custom transaction fee, if your business is processing over $250K annually in card payments.

“I’m very anti-surcharging… I understand that there might be a day when I have to start… but I think it’s more important to negotiate with the payment provider. With Zeller, we negotiated a great rate. I think it's on me to provide good service and that’s one way that I do it.”

Adele Arkell, owner of Radio Mexico, St Kilda, Melbourne

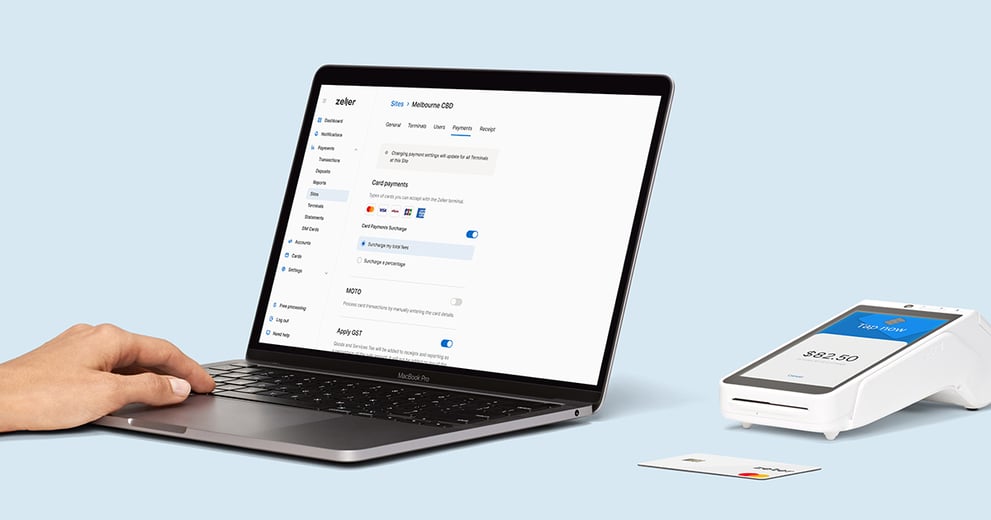

If you’re already using Zeller, surcharging can be enabled simply by toggling on the feature on Zeller Terminal or on your Dashboard.

If you are not using Zeller, you will need to check with your bank or payment provider. Bear in mind, some merchant services will only allow you to enable surcharging if you can meet minimum turnover thresholds every month, or will require you to sign a contract that locks you into using the functionality.

At Zeller, we believe in giving merchants the flexibility to run their business in the way that suits them best. That means having the ability to pass on your EFTPOS transaction fees in full or in part, and to turn the functionality on or off whenever you want to. There’s no contract to sign, or hoops to jump through.